US Corn Ethanol Market | an interview with Carl Zulauf

Ethanol was a factor in both the price run-up that began in 2006 and the price run-down that began in 2013. Tepid growth replaced explosive growth. The question for the future is, “What is ethanol’s organic growth rate (growth without government policy stimulus)?” Recent history suggests growth will continue in the corn ethanol market, but it likely will be notably lower than the growth in yields. Thus, upward pressure on corn prices is less likely.

Corn Ethanol in Historical Perspective

US Department of Agriculture data on US corn processed into US ethanol begin with the 1980 crop. It is reported monthly in the World Agricultural Supply and Demand Estimates. Corn processed into ethanol grew at an average annual rate of 6% between 1985 and 2000, exploded to a 24% annual growth rate between 2000 and 2010, then slowed to 1% per year after 2010 Ethanol Growth vs. Yield Growth. The explosive growth in the first decade of this Century largely coincides with the impact of government policies. These policies first led to the use of ethanol as an oxygenate additive in gasoline, then to the use of ethanol as a substitute for gasoline and by extension oil The latter was accomplished through mandates on market size enacted by Congress in 2005 and 2007.

Return to Equity for Processing Corn into Ethanol

Since January 2005, Iowa State University has issued a monthly report on the costs and returns to processing corn into ethanol. The report is based on (1) a model plant created using best available information and (2) current prices for corn, ethanol, natural gas, and distillers dried grain. Among the measures calculated is a return on equity. Figure 2 reports the average of monthly returns to equity by crop year. Even though growth in the ethanol market slowed dramatically after 2010, average return on equity remained positive for the 2011–2015 crop years (13%). As expected, return on equity was higher for the 2005–2010 crop years (30%). For additional discussion of the return to processing corn into ethanol, see Irwin, 2016.

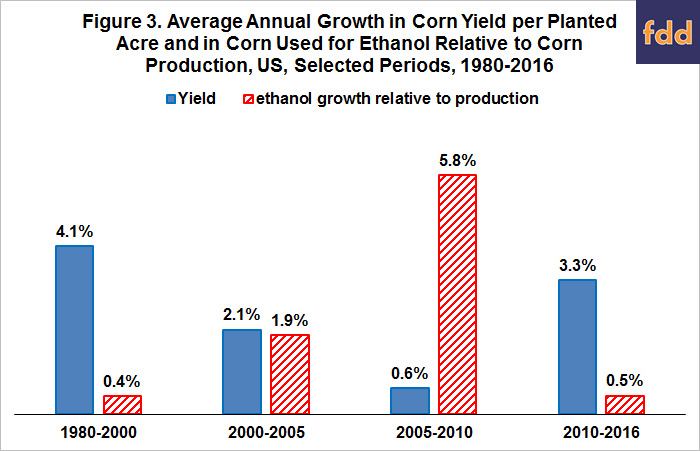

Ethanol Growth vs. Yield Growth

A measure of growth in demand (growth in corn processed into ethanol expressed as a percent of corn production) is compared with a measure of growth in supply (growth in US corn yield). To illustrate the calculation of these measures, 3.71 billion bushels of corn was processed into ethanol in the 2008 crop year, 0.66 billion bushels more than processed in the 2007 crop year. US production of corn in 2007 was 13.04 billion bushels. The growth in corn processed into ethanol was +5.1% of 2007 corn production (0.66/13.04). US yield of corn per planted acre was 151 bushels in 2008 vs. 149 bushels in 2007. Rate of growth was +1.3% [(151/149) - 1]. These two measures were calculated for each crop year.

Yield growth strongly exceeded the growth in corn used to produce ethanol relative to corn production before 2000 and after 2010 (see Figure 3). The two measures increased at about the same rate (2%) between 2000 and 2005. Between 2005 and 2010, growth in corn used to produce ethanol relative to production strongly exceeded growth in corn yields. Not only did corn processed into ethanol increase dramatically during the latter period, but the growth in corn yields was also abnormally low. Reinforcing these bullish price factors was China’s rapidly growing demand for soybeans (see Zulauf, 2016).

Summary Observations

-

From the perspective of 2016, expansion of the US corn ethanol market was largely squeezed into the 10 years from 2000 to 2010 (83% of the expansion occurred in these years).

-

The squeeze was largely driven by US policy decisions.

-

At the same time that policy was strongly pushing demand, growth in corn yields suddenly slowed, with a likely explanation being a multiple year period of suboptimal growing conditions.

-

However, the increase in demand for corn ethanol spurred by policy would have exceeded the growth in yield even during the high yield growth period of 1980 to 2000.

-

The result was not just an increase in corn price but an explosive increase in corn price.

-

This price increase increasingly looks unsustainable as yield growth returns to a path closer to history and ethanol growth returns to a level more consistent with long term organic growth due to market incentives, not policy factors.

-

If the preceding point holds, agriculture will need to make painful adjustments as it enters a world that will likely look more like 1980–2000 than 2005–2010.

-

Nothing in the historical review suggests that the corn ethanol market would not have developed. The continuing positive return to equity since 2010 suggests the market is sustainable. In particular, ethanol appears to have carved out a role as a competitive source of octane for gasoline, which is translating into a growth in exports of ethanol. For additional discussion of this topic, see Irwin and Good, 2016. But, annual organic growth is slower and unlikely to exceed the growth in yields.

-

This 35 year story does however raise caution about using policy to expand markets.

-

In particular, the design of such policy needs to respect the underlying private market, including attributes such as sustainable non-publically subsidized growth; role of competing demand components, such as livestock in the case of ethanol; and the scope and magnitude for supply growth to be uncertain and how this uncertainty may interact with policy induced demand growth.

-

Interesting, important, but probably unanswerable questions are what would be the current state of the corn ethanol market and by extension corn prices if government policy had not intervened and more narrowly if the 2007 mandate had not been enacted. The answers to these questions may tell us more about the future of corn and other field crop prices than any other set of questions.